Aug 2020

Aug 2020

Weekly markets round-up for StoneX Bullion

By StoneX Bullion

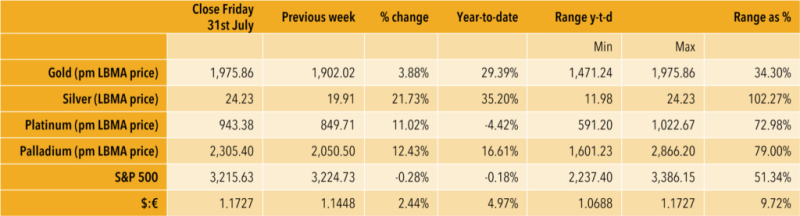

Welcome to a very brief overview of the recent performance in the markets. The essentials are captured in the table below and each week we will show a chart of interest.

Gold continues to make new highs while silver is its usual dangerous self

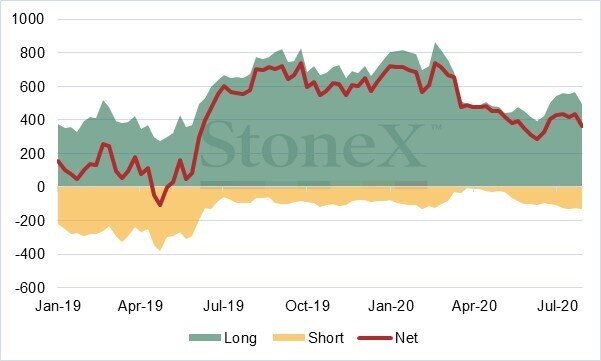

With $2,000 in view, gold continues to make headlines not only in the financial sector but also in the broader media. At the time of writing the high so far today is just over $1,990 and gold is still in overbought territory although the slowing momentum over the past few days has taken some of the heat out of the action. Interestingly, the Commitment of Traders figures for the week to the close of business last Tuesday, when gold closed at $1,958 (after a weekly gain of $147 or 6.4%) showed both long liquidation and increased shorts (see the chart below) among the Managed Money component. Clearly there was profit taking setting in towards the end of the month and after such a swift move; this week’s numbers will be instructive and may well show short covering.

Elsewhere in the market, the buying of gold ETFs has continued unabated, with the stream of purchases now extending to 25 consecutive days; of the 152 trading days so far this year, 128 of those have seen gold going into the funds. This is based on Bloomberg numbers, which are not quite as wide-ranging as the World Gold Council (WGC), which tracks over 140 individual funds. The most accurate number that we can currently show in terms of ETF activity in the year to date, therefore, is the latest figure from the WGC, which shows +864 in the year to 24th July; plus the subsequent numbers from Bloomberg, which gives an additional 36t of the following week, making 900t net inflow for the year to date. To put this into context, mine production over that period would have been approximately 1,980t.

Basis last Friday’s London LBMA afternoon gold price of $1957.65, this values these holdings at $56Bn.

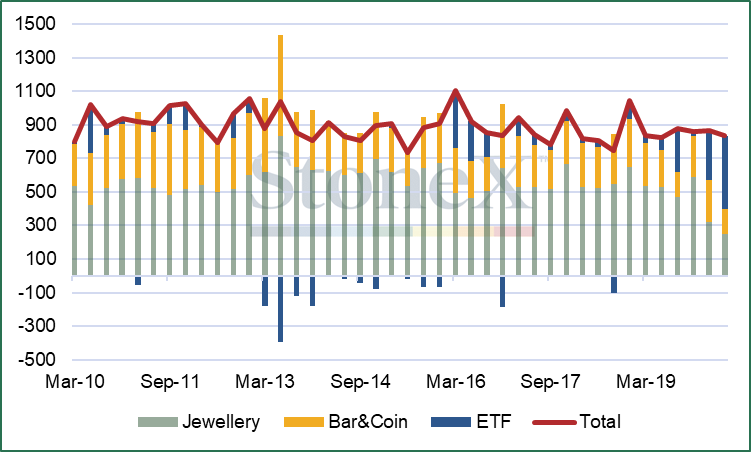

Meanwhile the WGC published its Gold Demands Trends for the second quarter, last Thursday 30th July, which showed that second-quarter global gold jewellery demand was just 251t, the lowest Q2 demand on record and compared with a quarterly average of 546t over 2018 and 2019. The bifurcation between East and West was even more stark than in the first quarter, with ETF investment, predominantly in the west, reaching 424t. If we take jewellery, ETFs and coin& bar demand together, the combined profile is much flatter, clearly showing how the demographics of the market have flowed; thus:

ETFs in the second quarter accounted for 43% of total demand in the second quarter (including industrial and net official sector activity), against an average of just 5% over the course of 2018 and 2019. Whether this momentum will be maintained through the rest of the year has to be questionable, but for as long as we have no clarity about the state of the virus’ activity globally then gold will remain in favour.

Chart for the week:

Gold managed money positioning on COMEX, net 364 tonnes as of Tuesday 28th July