This week we are doing something slightly different for our final note before the Christmas break, taking a look at gold in a negative interest rate environment. We wish all our readers a very happy Festive season and a happy peaceful and profitable New Year.

The tone of Fed Chairman Jerome Powell’s press conference last week was calm and looking towards a favourable economic outlook for next year, despite “global developments and ongoing risks”, which is a more bullish tone than over the rest of the year; he noted also that the Fed’s intention during the year to cushion the economy has been working. The Fed, on the basis of its median forecasts, is expecting real U.S. GDP to grow by 2.0% in 2020 after 2.2% this year, with unemployment holding steady at 3.5% and PCE inflation, the Fed's preferred inflation indicator, at 1.9%.

U.S. rates therefore remain in positive territory, but in Europe and Japan the picture is different and has been since the ECB pushed rates into negative territory in 2014 and Japan similarly in 2016. The global size of the bond market currently yielding negative returns is approximately $17Tn. Here therefore we take a quick look at what this means for gold; the hard numbers back up the theory, in part, as they show a dramatic increase in investment in Europe since rates moved below zero.

There are both positive and negative implications for the gold price in an environment of negative interest rates.

On the positive side

Negative interest rates obviate the argument about the opportunity cost of holding gold as it does not generate a yield;

Negative interest rates can be the precursor to the return of inflation and potential acceleration thereof—but before that they reflect governments’ intention to try and encourage the population to spend rather than save.

Negative interest rates reflect weak economic activity and associated systemic risks with investors so risk-averse that they will be prepared to shoulder the cost of holding bonds as a risk hedge.

And a high risk environment works in gold’s favour as one of the primary hedges against risk given its role as a portfolio diversifier and low to negative correlations with many major asset classes.

On the other hand

Negative rates reflect slow economic activity, which impinges on physical demand.

And the return to a positive interest rate environment brings the opportunity cost argument back into the frame.

So does the physical evidence back up the theories?

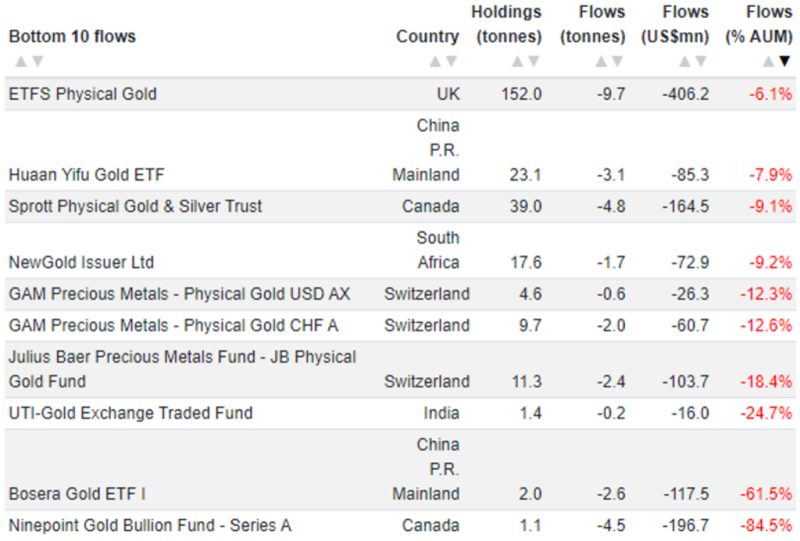

World Gold Council figures for coin and bar purchases in Europe from 2014 onwards do not show a headlong rush into gold in response to interest rates moving below zero, but this partly reflects the fact that consumers have been exercising caution in the face of economic slowdown. On the other hand, however, as the tables above from the World Gold Council show, European ETFs have at least in terms of percentages been dominating ETF inflows this year and among the Europeans, only Swiss funds appear in the bottom ten.

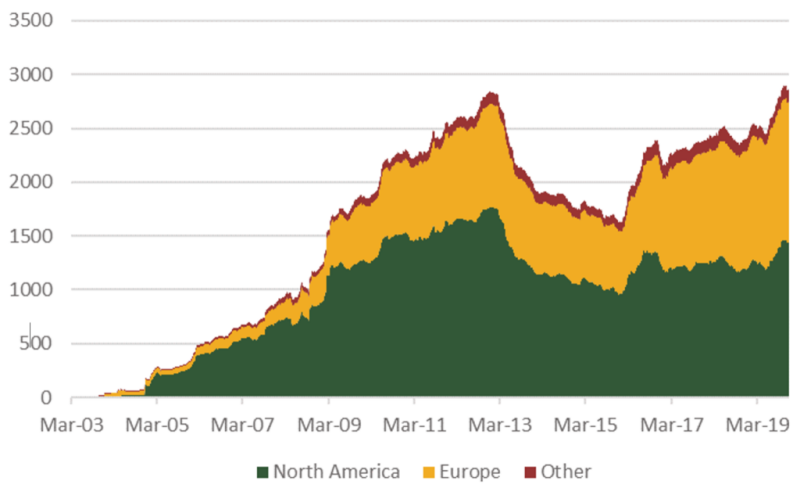

European ETF investment surges since rates became negative

What is particularly interesting, though, is to take the analysis to a more granular level. Daily figures collated by the World Gold Council show that since the start of 2015, tonnage holdings in North American gold ETFs grew by 403t or 39%; in the rest of the world bar Europe, the growth was 33t or 74%. In Europe, however, the holdings have risen by 685t or 111%. At end November European funds held a total of 1,306t against 1,441t in North America. See the chart on page three. Obviously negative rates are by no means the only driver of gold investment as they are part cause, part effect as outlined in the bullet points above. But they certainly help.

Gold ETF holdings by region; tonnes

Source: World Gold Council; INTL FCStone

Exchange Traded Funds — top and bottom flows in 2019, year-to-date

Source: World Gold CouncilSource: World Gold Council