Jun 2021

Jun 2021

Weekly markets round-up

By StoneX Bullion

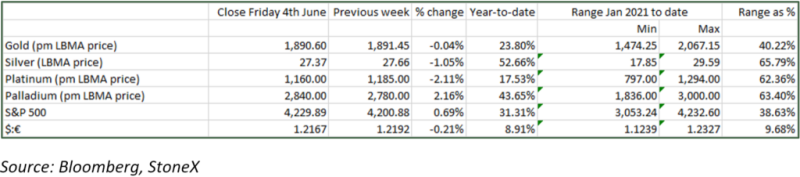

Welcome to a very brief overview of the recent performance in the markets. The essentials are captured in the table below and each week we will show a chart of interest.

When we wrote this column a fortnight ago gold had enjoyed a bull run since the start of May and was moving towards $1,900. We noted that gold was in overbought territory and in need of a correction as the market was becoming somewhat congested. That correction did ensue, but not for another week, peaking at $1,917 on Tuesday 1st June. This was its highest level since the first week of January; thus unwinding the losses that had been sustained since the start of the year, basing out at $1,677 a level tested three times during March.

Some of the falls last week, generally prompted not just by overbought conditions but also triggered by economic and financial developments in the United States, seemed in isolation to be quite sizeable, but when set into the longer-term context they were not that dramatic (see first chart below).

Later in the week the price sustained a fall of $45 (2%) in response to a U.S. unemployment report that was better than expected at 5.8%, below the psychologically significant 6%., as was the private payrolls figure for May, and with the service sector figures reaching a record. The U.S. ten-year yield, which is one of the key parameters influencing short-term gold moves, rose accordingly, from 1.59% to 1.63%.

These moves were partially reversed when the Nonfarm Payroll figure again missed market expectations. Nonetheless they were substantially better than the April number, posting a gain of 559,000. Payroll employment is still down by 7.6 million, or 5.0% from the pre-pandemic employment peak of February 2020, and unemployment stands at 9.3 million, compared with 5.7 million in February 2020. The participation rate (the percentage of the workforce that is actively looking for work) was steady at 61.6%, 1.7% lower than in February 2020.

Subsequently, the U.S. Treasury Secretary Janet Yellen, herself a former Chair of the Federal Reserve Board, has added her voice to those who believe that the U.S. inflation is transitory – although she was looking for inflation to head towards 3% over the course of the whole of this year. She also said that “if we ended up with a slightly higher interest rate environment it would actually be a plus for society’s point of view and the Fed’s point of view”. This had a fleeting negative effect on gold market sentiment, but this was short-lived, given that she made the comment in the context of wanting President Biden to push on with his $4 trillion spending proposal even if it triggered longer-lasting inflationary forces – and also the fact that U.S. CPI in May was 4.2%. But we must bear in mind that twelve months ago the economy was still massively dislocated as the pandemic took hold.

Meanwhile inflation in Europe has now reached 2%, but core inflation (in the EU this excludes food, energy, alcohol and tobacco) is just 1.2%. The ECB’s next policy meeting is 10th June and the market Is not expecting any policy changes.

Gold approached the peak last Tuesday 1st June and the Commitment of Traders report for the week to that date shows an eleven tonne increase in outright gold long positions, with a very small increase in the short position; thus taking the net long to 342t. This is not a massive overhang; the average since the start of 2019 is 372t.

On balance, then, gold continues to enjoy stronger tailwinds than headwinds with many real interest rates around the world firmly in negative territory (apart in particular from China) and continued geopolitical risk. Professional money managers are still looking at gold as a risk diversifier and at a retail level demand for silver coins, in particular, in the United States and Europe is very strong and coins are in short supply.

Gold unwinds its overbought condition and moves to more sustainable levels

Gold, the U.S. ten-year yield and the correlation between the two