Sep 2021

Sep 2021

Gold and silver still fluctuating, no discernible trend

By StoneX Bullion

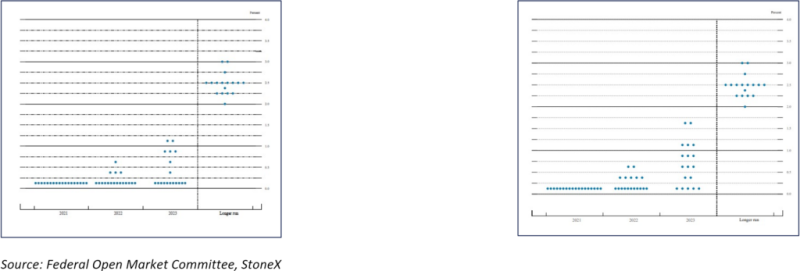

We have noted frequently that while inflation may be the current focus of the markets’ attention, it is not necessarily the key driver for gold prices. In the present environment, with the delta variant still ebbing and flowing, the possibility of the economic recovery being derailed is a concern and therefore, once again, we have to monitor the nuances coming from the members of the Federal Open Market Committee. The next meeting of the Committee is next Tuesday and Wednesday, the 21st and 22nd of September and the tone is becoming increasingly hawkish. This meeting is one of the four during the year in which economic projections are published, including the “dot plot” which charts each member’s expectation for the level of the federal funds rate at the end of this year, next year, and thereafter. The charts below show how the expectations changed between March and June. The increased hawkish tone sent a big ripple through the markets; this time any similar change will probably have a lesser effect since it has been the topic of much market commentary over the past few weeks.

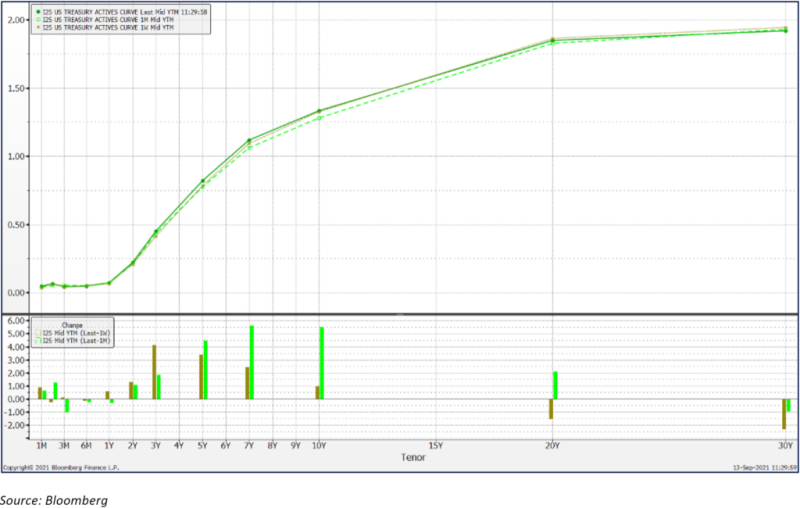

As a result the release on Friday last week of the August Producer Price Index was higher than expectations at 8.3% year-on-year; gold’s resulting fall reflects the fact that the markets are still concentrating on the prospect of tapering from the Fed and the potential for interest rates to edge higher. Interestingly, the U.S. yield curve is flattening ever so slightly at the longer end of the maturities, while strengthening in the short term (as far out as ten years), suggesting that the markets are pricing in a reasonably solid economic recovery; this also helps to explain why gold is holding to a neutral pattern.

To some extent, though, this is counter intuitive. Nominal interest rates in the United States are, though positive, still extremely low and real interest rates are negative virtually globally. Meanwhile the Fed’s and European Central Bank’s combined balance sheets have expanded since the start of 2020 by $7.5Tn, or 85% (the Fed’s balance sheet has doubled and the ECB’s by 72%); this is equivalent to the combined 2020 GDP of Germany, the U.K. and the Netherlands, or the third largest GDP globally (numbers from the World Bank). In principle this should argue for high and rising inflation, but the economic risks stemming from the persistence of the COVID-19 virus are keeping matters in check.

A lot of this excess liquidity has gone through to the consumers (unlike in the Global Financial Crisis of 2008, when the banks were required to bolster their balance sheets in order to renew stability) and this has helped to bolster the economic recovery, but there is still excess liquidity in the system that is looking for a home. Gold has been one of the targets, as a hedge against risk. It is arguable that without this activity the price could be lower than currently, especially as the physical markets appear to have stalled. The Middle East in particular is very sluggish at present.

Given the environment, with gold essentially trading sideways, silver is underperforming, with the ratio now at 75.6, up from 73.7 a week ago. This makes sense, since silver, with a lack of guidance from gold, is looking at the industrial outlook and the virus-driven uncertainty is keeping sentiment neutral to mildly bearish. There is a substantial amount of pent-up demand waiting in the wings in India in particular, but the market is still very cautious. The shortage of shipping capacity is also keeping silver on edge as some shipments are now having to go by air. Freight rates are also incredibly high (the China – U.S. West Coast rate has risen by a factor of 13 since June of last year), which is also feeding through to inflation numbers – and here, too this is a transitory effect.

These markets, barring an exogenous shock, are likely to remain range bound until the FOMC meeting. Although it has been a topic of conversation for weeks, it will, nonetheless, be a key driver for market direction in the near term.

The Fed’s dot plot, March and June

The U.S. yield curve, today, a week ago and a month ago; changes are shown in the lower panel