Aug 2021

Aug 2021

Gold more resilient than the headlines suggested last week

By StoneX Bullion

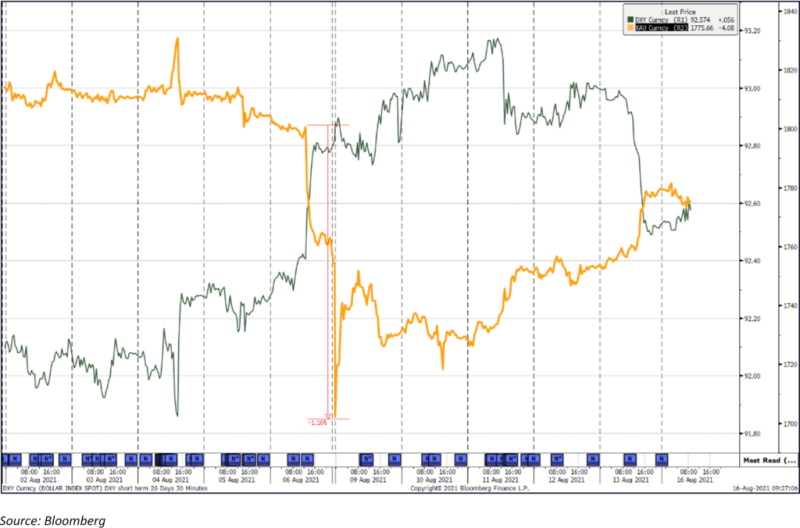

Last Monday saw gold captured the headlines with a sharp fall in price at the start of Asian hours’ trading. The price had already been on the retreat the previous Friday after strong U.S. employment data lifted the dollar and reignited expectations of early tapering from the Fed – although that has now been reversed (see below). As Asia opened on Monday gold dropped sharply in a very short space of time.

While the outright price action drew the attention of the press, with spot falling from $1,800 on Friday to bottom out at $1,691, the retreat was only 1.1%, which puts it into a better context. It is not clear what happened, but the move coincided with a gain in Treasuries and the general market view is that this was a shift out of gold and into U.S bonds on the part of one fund. The negative nominal interest rates in a number of countries, especially in Europe, mean that U.S. bonds have been in demand of late, even if the ten-year yield is below 1.5%.

The physical gold market came to life in response to the price fall, with Shanghai moving to a premium of $10 over loco London, and interest building both in India and the Gulf Cooperation Council countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE). Parts of the Far East are also livelier, although the impact of the pandemic is still keeping some areas out of action. As we write gold has recovered to $1,778, so over 80% of the fall has been unwound.

It will be interesting to see what the CFTC number show us for the COMEX positioning in the recovery week. What we did see in the aftermath of the price fall was instructive. The CFTC reporting week ends on close of business on Tuesdays, so the market activity from last week’s numbers neatly encapsulates what happened during and after the price drop. Naturally there is bound to have been stop-loss and momentum trades triggered and the volumes were telling. The gold contracts dropped 65t of long positions, equivalent to 16% of the outstanding position the previous week, while shorts added 104t, or 78% of the previous week’s level. There is little doubt that some these will have been covered thereafter. The current net positions are just 110t for gold, the lowest since March, and 2,070t for silver, the lowest since May 2020.

The silver position was similar, with long liquidation or 863t (8%) while shorts expanded by 1,465t or 37%. Silver’s fall was 11%, from $25.50 to $22.63, but while gold has unwound a good part of the drop, silver has only recovered 34%. Silver’s industrial base is currently more influential than its relationship with gold as the markets fret about the spread of the delta variant of the virus. As noted above, the markets are also now starting to think that the Fed will delay tapering, or at the very least, not bring it forward. The University of Michigan Consumer Survey, one of the more influential elements among U.S. economic drivers, was released last Friday and was way below forecasts, with current conditions index dropping to 77.9 from 84.5 in July and the expectations index dropping to 65.2 from 79.0. The one-year inflation index came in at 4.6% and the five-year expectation was 3.0%.

In addition the bond market is suggesting that the markets are sanguine about the inflationary outlook, with the ten -year breakeven inflation rate below the five years, at 2.36% and 2.50% respectively.

Managed money positions in the COMEX gold contracts

Gold and the S&P 500 index