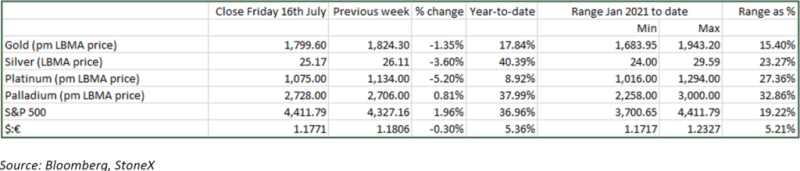

Jul 2021

Jul 2021

Gold down last week but reasserting in risk-off ode this morning. Mixed emotions.

By StoneX Bullion

Last week saw gold stage its first weekly decline since the big clear-out after the Federal Open Market Committee (FOMC)’s mid-June meeting, but while this fact is catching the headlines the bigger picture shows gold continuing in a period of consolidation in a narrow range centred on $1,800. The technical construction on the chart suggests that it is due a break-out in one direction or the other. The ten-day moving average is closely hugging prices to the upside and offering resistance accordingly, while the 20-day average is performing the same service in support. At the start of the week the markets have generally moved into risk-off mode, with (as usual) gold and U.S. Treasures the major beneficiaries.

The primary influence last week was a mild strengthening in the dollar, but the movement was relatively constrained. June housing starts for the United States were reported last week and were strong, but May building permits eased, which suggested that the recovery may have been losing some steam – which arguably it needs to do given the rapid pace of the turnaround in recent months. The Leading Economic Indicator, released later in the week, was strong and now stands 3% above the levels prior to the pandemic.

These latest numbers suggest that the debate among members of the FOMC will be as lively in this week’s meeting (27th and 28th) as it was in June. The activity in the bond market at the end of last week in response to the economic numbers was dovish, to the extent that the bond market is now discounting no rate hikes until the end of 2022 – previously the expectation was more like the middle of the year.

This is supportive for gold

On the other side of the market, however, ETF activity, which is closely watched because of its transparency, has put something of a cloud over the market, with only four days of inward investment so far in July; the net change over the month has been a fall of 20t and a net dollar outflow of $1.1Bn. This also tends to attract headlines and so passing market observations are torn between positive financial factors, but an erosion in investor interest, albeit mild.

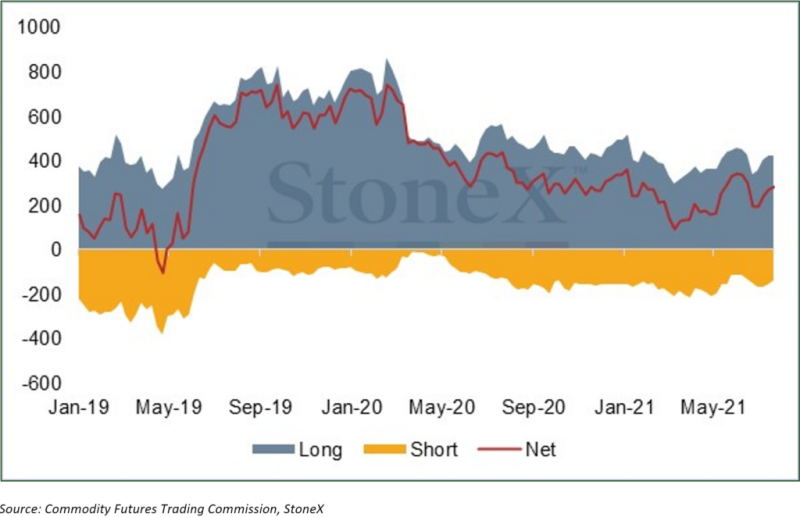

So what are the futures markets telling us? Effectively they are reflecting the mixed emotions in the market. In the week to Tuesday 20th July, before the Leading Economic Indicators came out, the outright Managed Money long positions declined by three tonnes, a fall of less than 1%, while shorts contracted by 16t or 10%.

The markets are focusing closely on the FOMC meeting, which is likely to keep gold quiet until midweek. This meeting does not have economic projections tied to it (the next is September 21-22), but the Statement and Jay Powell’s Press Conference will be closely scrutinised. We would expect that there will be no real change from the June meeting – but the markets are likely to remain sclerotic ahead of it, nonetheless.

Probably of more import is Friday, when we have the U.S. Personal Consumption Expenditure numbers and possibly even more influential will be the China Purchasing Managers Index figures, also on Friday. This brings us full circle to the start of this week; the reason why the markets went firmly into risk-off mode came from the Chinese Government’s announcements over the weekend that it is clamping down on the country’s private education companies that teach school curricula, preventing any such companies from making profits, raising capital or listing publicly. Among other changes, overseas investment is now prohibited in such companies. The relevant equity sectors plummeted, and other markets have suffered some contagion, taking the markets firmly into risk-off.

Managed money positions in the COMEX gold contracts

Gold and the U.S. ten-year yield