Feb 2022

Feb 2022

Fresh gains on geopolitical tensions

By StoneX Bullion

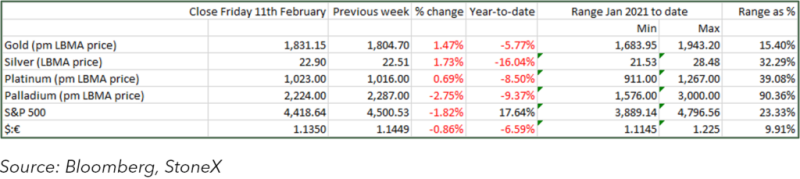

When we last wrote a fortnight ago, gold looked as if it had [presented us with a “false dawn”, breaking out of its six-week long range, but falling back again relatively quickly. Since then, as the markets focus increasingly on the tensions over the Russia/Ukraine border, prices have been climbing steadily, to touch highs last Friday (11th February) of $1,865. By this stage the market was overbought on both the Bollinger Band and Relative strength parameters and so as we write today (14th February) it is taking a much-needed pause for breath.

Gold has taken silver with it, rising from $22.60 to $23.62. The gold:silver ratio has contracted accordingly (it usually does in a bull phase, as silver is more volatile than gold), coming in from just over 80.3 to trade most recently at 78.3.

The concerns over the amassing of Russian troops on the Ukraine border and increasingly intense diplomatic activity have been cornering the headlines in the press and helping to support gold prices on the back of geopolitical risk. The latest figures from the Commodities Futures Trading Commission show that in the managed money sector (largely fund managers) show that in late January the markets were in bearish mode, but in the week to 8th February the mood changed, with long-side positions increasing and short covering developing in gold; in silver the tone was less convincing, with longs taking profits and only mild short-covering in the second week, after a big increase the week previously. Meanwhile the Exchange Traded Products are taking in metal, with gold posting gains of eleven tonnes since the start of February, for a year-to-date gain of 47t and a net dollar inflow of $3.1Bn.

In the economic background, the markets were also looking for the United States’ CPI figure, released last week, which cane in at +0.6% month-on month, with food and energy both at +0.9%, but fuel oil still rampant at 9.5% (although it had declined in December). Core inflation, which the Federal Reserve tends to prefer to watch on the basis that food and energy are both volatile, was also up by 0.6%. This was broadly in line with market expectations. Inflation itself is less of an issue than the Fed’s attitude to controlling it and Jay Powell and other members of the Federal Open Market Committee have recently been unwavering in their determination to bring price rises down towards the 2% year-on-year target; the markets have therefore effectively priced in a rate hike in March. What is still a cause for debate is whether it will be 25 or 50 basis points. Experience would suggest that the Fed’s cautious attitude and intention to maintain flexibility would tend to suggest that the smaller hike is the more likely.

The next Commentary will be on Monday 7th March

Gold, Silver; their correlation and the Ratio

Gold and the VIX Index

Gold in Dollar, Euro and Rupee terms — Independent Strength