StoneX Bullion round-up Monday 24th October 2022 and a link to part of the LBMA/LPPM Conference

By StoneX Bullion

Metals

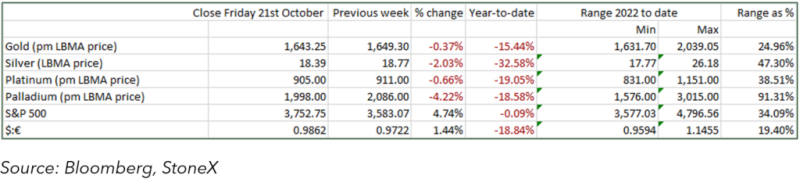

Gold has largely trended lower since we last wrote a fortnight ago, easing from $1,680 to a low late last week of $1,620; it has, however, found some support since and, as we write, spot prices are holding above $1,640.

Silver followed suit, easing from just over $20.60 before consolidating between $18.20 and $1,850, forming what looks like a reasonable base.

Taking a longer-term view, it looks as if gold and silver have both been forming a base during September and October, possibly reflecting views held in some quarters that the dollar’s strength (it briefly hit a 32-year high after the CPI numbers) may not have much further to go.

Gold and silver, 2022 to date

That certainly appeared to be the view of the view of Peter Zöllner, the Head of the Banking Department at the BIS, when he spoke at the LBMA/LPPM Conference last week.

Meanwhile one of the key topics of conversation at LBMA/LPPM was the silver market and the massive flows of metal that have been coming out of LBMA, COMEX vaults plus ETPs (over 12,000t year-to-date), feeding renewed Indian demand after two awful years, and in the face also of reduced selling from Chia of late. Please see a full piece on this herein the Market Intelligence portal.

The overall tone seemed to be downbeat as far as gold was concerned, but despite that the Conference consensus was, at the start of the meeting, that the price this time next year would be ~$1,850; at the end of the Conference the expectation was just over $1,830. So a slight toning down, but still bullish overall, for a gain of more than 12% year-on-year.

Background

U.S. inflation figures on 13th October showed a headline CPI of 8.2% year-on-year, reflecting rising rents, which gained 7.2%, extending a rising trend as the home-ownership market totters, while food prices were up 11.2%, with the largest increases coming in grain-related products. Shelter overall (ownership and rental) comprises 32% of the U.S. CPI.

The dollar strengthened in immediate response to the inflation numbers, but has eased since then, helping to give gold some support, although there is a body of resistance on the charts reaching up from $1,670 to $1,680, which may impede any fresh attempt on the recent highs just above $1,720.

Market developments

In the background the gold Exchange Traded Products are still losing metal. Apart from a very small inflow of just 300kg on 18th October, the gold ETFs have continued to contract. Since the start of September holdings have dropped by 149t to 3,501t. This means that year-to-date the gold ETFs have lost 71t. extending the reverses from the strong gains driven by U.S. and European purchases in the wake of the invasion of Ukraine.

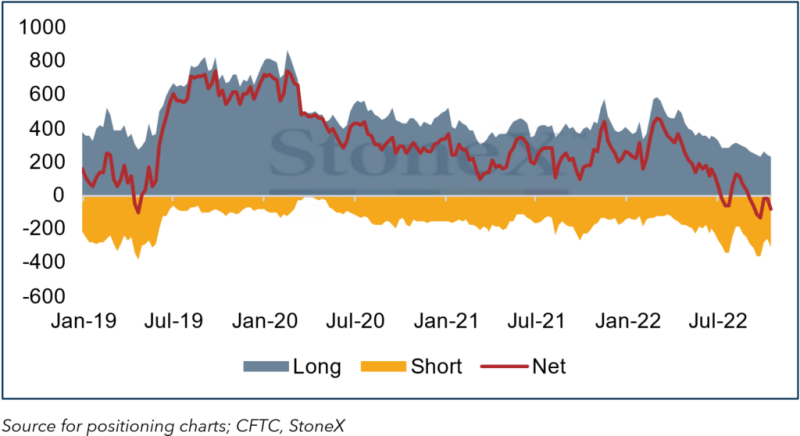

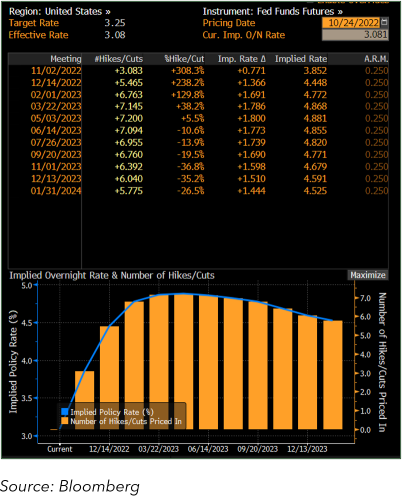

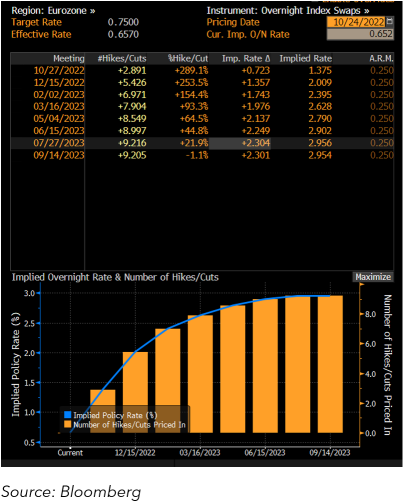

On COMEX, gold’s weekly price moves to 18th October (a drop from $1,681 intraday high to $1,652) saw the net short increase again, on the back of light long liquidation but a quite aggressive increase in shorts. Doubtless some of this came through in the wake of the stronger-than-expected U.S. inflation data, which brought the hawks out again, but not in such force as in previous months. It is possible that the markets are starting to incline to the view that two more 75-basis point hikes are priced in and that there may be an increasing chance of a pause thereafter. The fed funds markets (see the charts below) are still pricing in an interest peak in the US in May, at 4.88% while by contrast, the EU markets are looking for a peak a lot further out.

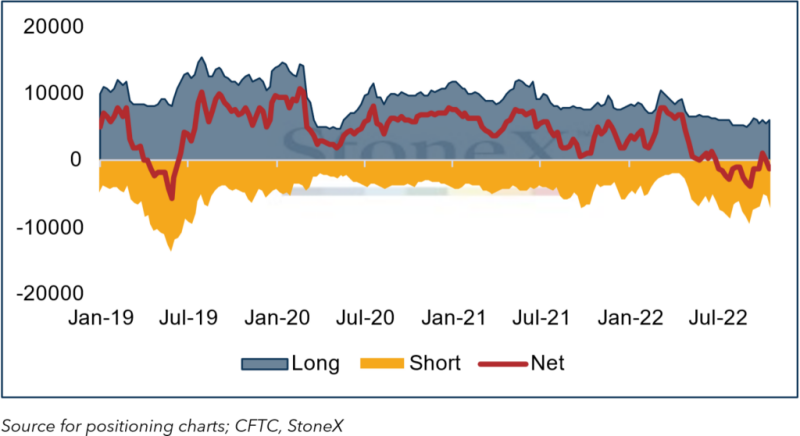

Silver also swung into a net long, with 556t of fresh longs (an increase of 10%) and short covering of 1,562t or 24%. The net position thus went to a long of 906t from a net short of 1,301t, after 13 weeks of net shorts, while silver ETFs have started to see some bargain-hunting. Since the start of September (38 trading days), 14 days have recorded net inflows, and five of those days have been since 13th October, for a net gain over that period of 443t. For the year-to-date the silver ETFs have shed 3,997t.

Meanwhile since end-September gold open interest on COMEX has increased slightly, while inventories have come down 23t to 796t, comprising 58% of total open interest. In the silver contracts, open interest has increased by 6% or 1,331t to 21,490t (a year’s global industrial demand is roughly 26,000t); inventories, at 9,458t, comprise 44% of total open interest.

Key charts

Gold in dollar terms, year-to-date; technical indicators. Out of the downtrend and jousting with the 10 and 20D moving averages

Gold, silver, the ratio and the correlation

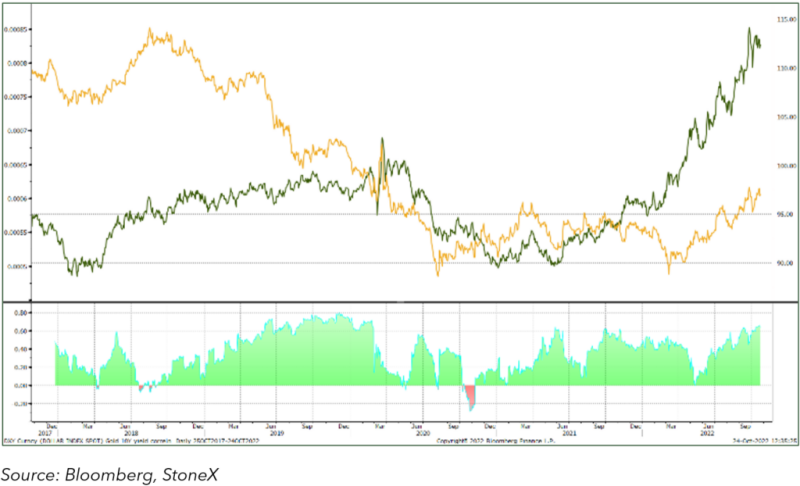

Gold (inverted) and the ten-year yield

Gold and the S&P; correlation

Gold and Silver COMEX positioning, tonnes

The bond market’s fed funds target projection; peak of 4.6% in May next year, up 20-basis points from a fortnight ago. Europe; not peaking until September, and maybe not even then