Oct 2022

Oct 2022

StoneX Bullion round-up Monday 10th October 2022 and a look at the Indian harvest

By StoneX Bullion

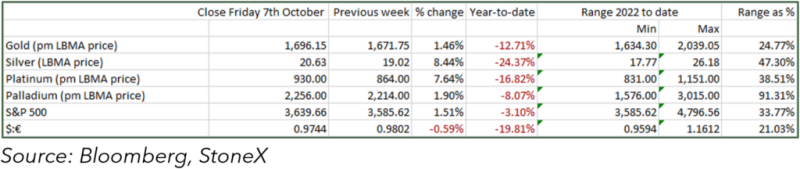

- Gold’s rally in the first week of October, which had already started when we wrote last week, continued until midweek when overbought considerations brought about profit taking.

- Strong U.S. employment figures put further pressure on the price as the Fed’s rate cycle came back to center-stage

- The previous downtrend was broken, and with gold currently challenging the 10-day moving average to the downside, that channel may be the next level of support (currently at $1,672).

- Silver’s rally was, as is normally the case, stronger than that of gold, but this time the move was roughly three times that of gold in percentage terms, as against a more normal beta of two to two-and-a-half times

Background:

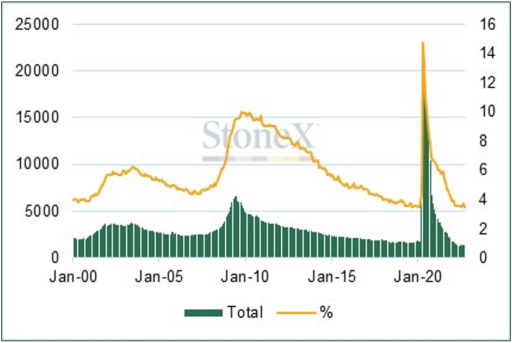

- The increase in nonfarm payroll figures in the United States was as expected, but the unemployment rate dropped to 3.5% after 3.7% the previous month; the markets had been looking for 3.7% this month also. This chart shows continuing jobless claims in 000s and percentage.

- There were notable gains in leisure and hospitality and in healthcare; the improvement in the leisure industry is helping to fuel inflationary expectations. Unemployment edged lower, to 5.8 million, while the labour force participation rate (the proportion of the unemployed population looking for work) was steady at 62.3%.

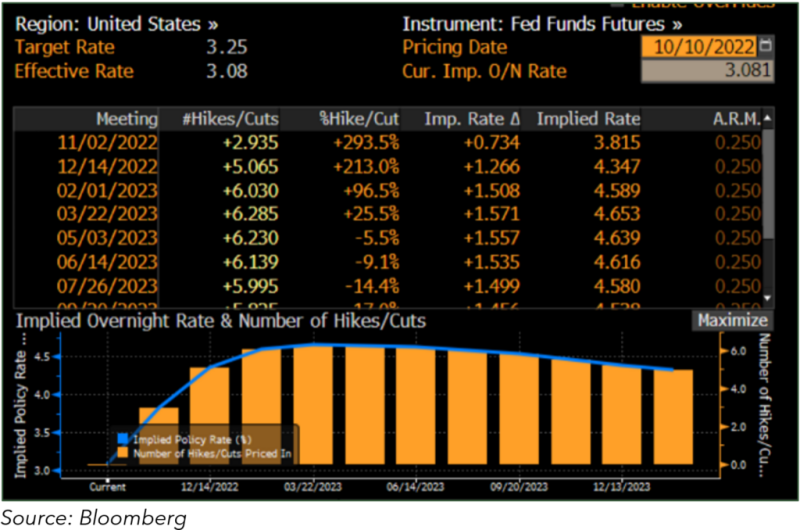

- The fed funds futures markets are now discounting a peak in fed funds of 4.65% in March of next year, which – although 20 basis points higher than last week - may still prove to be somewhat benign, given the inflationary undercurrents and the Fed’s determination to combat them.

- The ten-year yield, with which gold currently has a 0.6 correlation, rose almost a 0.1% in the wake of the numbers, also helping to put pressure on gold, but subsequently gave back part of those gains.

- Asian buying interest has helped to steady gold over the weekend, but spot prices are once again below $1,700 and trading at $1,680 as we write.

The Indian harvest and the gold market

The 24th of this month sees the start of the Diwali Festival, which is the most auspicious period in the Hindu calendar for gift giving, and gold normally features strongly in this celebration, as does silver. Some local jewellers are suggesting that, with the rupee where it is, silver may be more of a beneficiary than gold this year. The monsoon season has been a good one, which implies a good harvest. Now in India, roughly 40% of the population works in the agrarian sector and a total of 60% of the population is reliant on it to one degree or another. Farmers tend not to trust the banking sector and gold is one of their primary purchases. So the level of their disposable income is a function both of the size and quality of the harvest and the prices that it commands. This is largely in the hands of the Government, which sets a Minimum Support Price during the year.

This year the Cabinet Committee on Economic Affairs, chaired by the Prime Minister, approved price hikes for 14 Kharif crops, leaving all of them profitable on the basis of average prices, and contributing, on the Government’s calculations, to a gain of 15-20 basis points in local inflation. Kharif crops (of which Paddy rice is the most important) are sown at the start of the rainy season and also include maize and soybeans. The Diwali Festival follows that harvest, while Rabi crops are sown at the end of the monsoon (i.e. now) and include wheat and barley, oats, pulses. The Akshaya Tritiya Festival follows that harvest – and is challenging Diwali for top slot where gold is concerned.

So, an assessment of the strength of gold demand in India requires a degree of meteorological work!

Market developments

In the background the gold Exchange Traded Products continued to bleed metal. Last Monday 3rd October saw a small increase, but that aside the funds have been consistent sellers; of the last 50 trading days, only seven have been days of increased holdings. For the year to date, the funds have been net sellers of 30t, more than reversing the strong gains driven by U.S. and European purchases in the wake of the invasion of Ukraine.

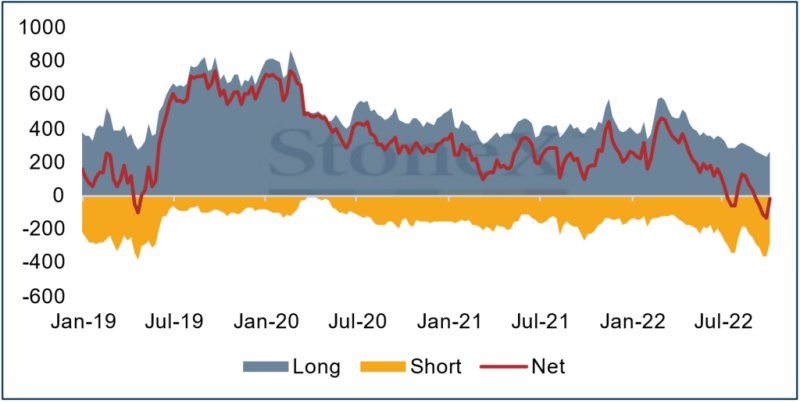

Meanwhile the price rallies of the first part of last week were indeed driven by activity in the professional markets with the managed money numbers from the CFTC showing a major swing to the long side in the gold market, with 27t of fresh longs and a heavy 86t of short covering, equating to a 12% increase in outright longs and a cut of 24% in the outright shorts. This took the net long to 113t after seven weeks of net shorts and compared with a twelve-month average of 192t.

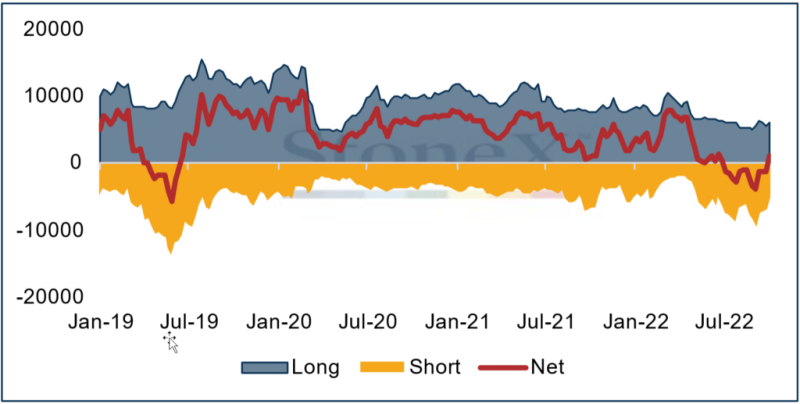

Silver also swung into a net long, with 556t of fresh longs (an increase of 10%) and short covering of 1,562t or 24%. The net position thus went to a long of 906t from a net short of 1,301t, after 13 weeks of net shorts.

Physical demand remains strong in the silver coin market and some orders are being booked through well into next year.

Key charts

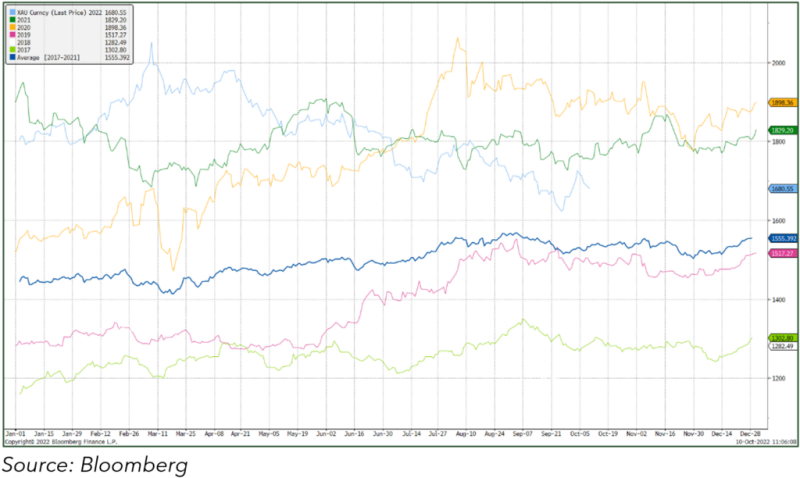

Gold in dollar terms, year-to-date; technical indicators

Gold in rupee terms, seasonality chart

Gold, silver, the ratio and the correlation

Gold (inverted) and the ten-year yield

Gold and the S&P; correlation

Gold and Silver COMEX positioning, tonnes

Gold: -

Silver: -

Source for positioning charts; CFTC, StoneX

The bond market’s fed funds target projection; peak of 4.6% in March next year. Too benign? Recent figures may suggest not