Sep 2022

Sep 2022

StoneX Bullion round-up Monday 5th September 2022

By StoneX Bullion

Don’t let the dollar’s strength confuse you

- Miserable gold generates even more bearish technicals, but is now oversold

- Silver is relatively stable given gold’s action; the ratio is down from 96 to 94, but still very high. Net short the largest since May 2019.

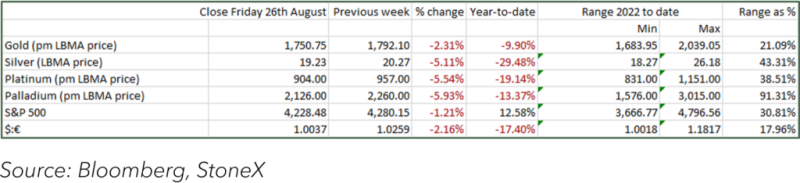

- Dollar remains strong but gold is now holding just above $1,700

- ECB rate decision due later this week

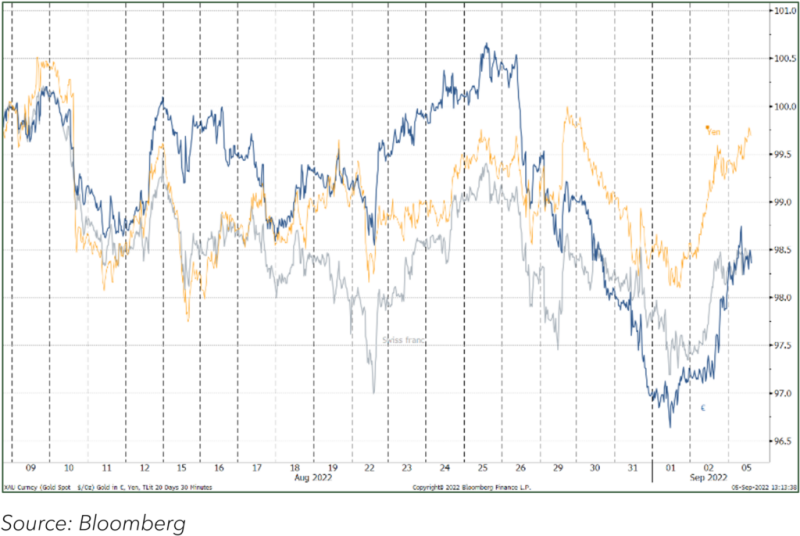

Geopolitical factors continue to intensify while there is still uncertainty over OPEC+’s next course of action in the oil market, both of which are supportive for gold; while the dollar has continued to strengthen, which has helped to contribute to gold’s limp recent performance. In fact if we look at gold in some other local currencies gold has regained some of its recent losses over the first part of the week.

Gold’s dollar-denominated fall to a six-week low of $1,688 essentially covered the whole of the second half of August, puncutated by a small correction between the 23rd and 25th. Overall, prices slipped from $1,805 (intraday) to just below $1,700 at the end of last week, from where it has found some light support. The trigger for the fall was, as we noted last week, additional hawkishness from the FOMC, possibly compounded by the cut in China’s prime rates. The subsequent bounce, if such it can be called, is partly a simple reflection of oversold conditions. Over and above that, however, the NonFarm payroll figures in the United States last Friday, while ahead of the market call, were much less aggressive than in July and prompted some thoughts that at the 21st September meeting the Fed might hike by 50 basis points rather than 75 (the meeting concludes on 21st September and will include the new dot plots, which will be interesting).

Gold in major local currencies, August and early September

The fed funds markets are pricing in a 50-point hike in September, and are looking for the rate cycle to peak in March with the fed funds target at 3.9%. Given that the latest CPI figure was 8.5% year-on-year it is arguable that the market is taking too benign a view of the Fed’s likely course of action over the next few months.

Meanwhile on the other side of the Atlantic the European Central Bank is facing inflationary headwinds and Christine Lagarde has made it abundantly clear that she wants it defeated. With the energy crisis in Europe, however and particularly with Nord Stream 1 (the key gas pipeline form Russian into Europe) still closed, the ECB has an uphill task in front of it. The markets are expecting a 75-point hike from the bank this week (meeting takes place on Thursday the 8th) and the latest inflation reading (August) was 9.1%, with Germany posting 7.9% and France, 5.8%. High rates are prevalent in southern Europe with Italy at 8.4%, Portugal 9.4%, Spain 10.4% and Greece, 11.3%. The bond markets are pricing in a hike of just under 75 basis points, so 75 is what we should be expecting; the curve is also suggesting that rates will continue to price at least through to the middle of 2023, where the rates are projected at 2.24%, compared with zero now.

So we are still presented with hawkish central bank activity in the face of inflationary forces that are to some extent borne of exogenous shocks and which therefore point to stagflation or the potential for recession.

Gold, the moving averages, the MACD and the RS

Generally gold does not perform too badly in a recession as its role as a risk hedge comes into play but at the moment the professional markets are treading with caution. The Commitment of Traders’ report shows that action in the week to last Tuesday 20th August, when gold was obviously still sliding, saw some light liquidation and a further increase in shorts, leaving gold in a small net long of 37t, compared with an average net long over the past twelve months of 218t. Silver saw some light liquidation but yet another big increase in shorts, to generate a net short of 3,381t, the largest since May 2019. If there is any shock to the markets that generates short-covering in silver (currently trading at $18.17), the move could be vicious.

Exchange traded fund stakeholders continue to sell off; in the 25 trading days since the start of August gold has seen just five days of creations, while silver has seen nine. Over that period gold has redeemed 49 tonnes and silver, 982t, contractions of 2% and 4% respectively.

Gold and the US dollar; correlation

In the background the physical markets have been picking up as prices have fallen, despite the dollar’s strength and Middle East and Turkey in particular (hardly surprisingly, given Turkey’s rampant inflation, currently at 80%) have been lively. Indian interest is also starting to pick up. Diwali, the most auspicious Fesitval for the giving and receiving of gold, starts on 24th October and we could well be seeing some bargain hunting ahead of the Festival.

So we are still watching the central banks. Surrounding factors are supportive for gold, but for the time being the professional market is preferring to sit on its hands.