May 2022

May 2022

StoneX Bullion round-up Monday 15th May 2022

By StoneX Bullion

The process of attrition in the gold and silver markets is continuing and the positioning in the COMEX contracts is theoretically rendering silver vulnerable to a short-covering move. Silver has been sliding lower along with gold. As we write gold is trading at just below $1,800, down 14% from its early-March high and at the lowest since end-January, just as it was starting its six-week bull run. Silver has picked up a little this morning and regained the $21 level but is down by 24% from its early March high of $26.94 (intra-day).

For now, though, sentiment remains cautious all round the markets as the war drags on in Ukraine, agricultural prices are soaring and the word “stagflation “, in Europe at least, is becoming increasingly commonplace. The Federal Reserve in the United States remains sanguine, with Fed Chair Jay Powell arguing that the economy is sufficiently robust to weather further sizeable rate hikes, although he has been making it clear that the Fed is not currently considering rate hikes of more than 50 basis points in any one meeting – at least not for now.

Europe; nominal and real interest rates

Even so the prospect of rising interest rates is unsettling the precious metals markets even though they should be well and truly discounted by now and real interest rates themselves are, except for China, negative in all the major economic regions.

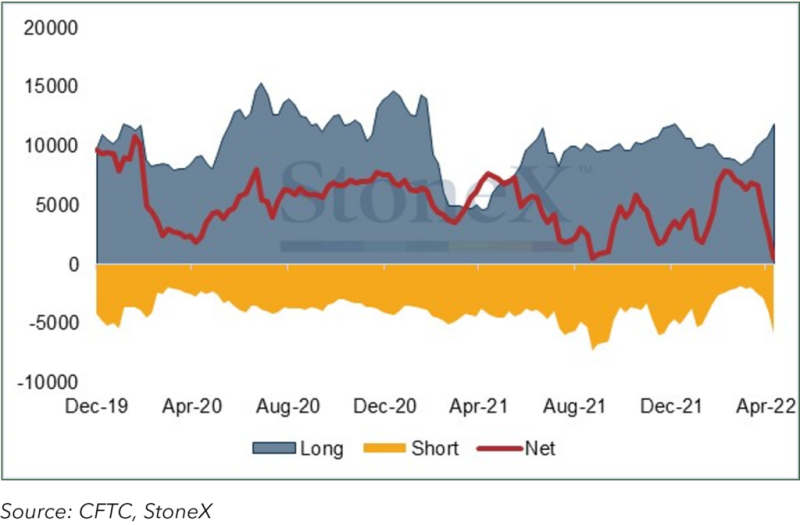

The outright Managed Money short position in silver as of last Tuesday 9th May (when spot was sliding towards $21) was 38,106t, the largest since mid-December last year and outright longs are at their lowest since May 2020, the net long position, at 1,846t, is the smallest since last September.

Within the Exchange Traded Products the picture is mixed (unlike gold where there has been continuous selling, see below); over the past four weeks silver ETPs have seen eleven days of redemption and nine days of creations. For the year to date the silver ETPs have achieved a small net addition of just 227t.

So far there is little sign of any bargain hunting in the professional market but the market for coins and bars at a retail level remains extremely lively with most mints on allocation and coins are commanding high premia. One sign of life is that the gold:silver ratio, which hit a 22-month high of 87.7 last week, has eased very marginally, but not to any degree of significance.

While sentiment remains nervous over the economic outlook and gold remains under some pressure then silver is likely also to remain under a cloud; a word of caution is necessary here, though as silver can be vulnerable to very sharp moves, especially when there is a short-covering rally involved. It is hard to see what might trigger such a move at present, but it is important to be vigilant in this market.

Gold, meanwhile, is also experiencing very strong physical demand in the Middle East, Turkey, and other parts of Asia, with domestic price commanding high premia also. The professional market is looking the other way, however. Since its recent high (1st March, spot at $1,950 en route for the 8th March peak at $2,080), the outright Managed Money long on COMEX has dropped from 582t to 386t, the lowest since mid-February this year.

Silver: Managed Money Commitment of Traders, tonnes

Among the Exchange Traded Products the last four weeks have seen 14 days of redemptions and only six days of creations. Year-to-date the funds have expanded by 227 tonnes to stand at 3,830t, just more than one year’s global mine production. This continued haemorrhaging does tend to attract market attention as it reflects institutional activity (silver ETPs have a higher retail components) and gold ETPs can often, on this basis, become price makers rather than price takers and it can certainly be argued that that is the case at present.